If you are like many other nonprofit bookkeeping specialists, you think about your Statement of Activities when asked about financial reports. This is also known as the Income Statement, or Profit and Loss.

It’s an easy report to focus on and share with your board since it tracks the ways money comes into and flows out of your organization.

But if you’ve ever had an audit, you may have noticed that the auditors don’t spend much time with your income and expense accounts. Sure, they want to know about contributions of $5,000 and above, and they’ll pay more attention to restricted or government grants.

They’ll make sure your salary expense lines up with your quarterly payroll reports. They may ask questions when there is a significant variance in any line item year over year.

But they’ll spend most of their time digging into the details of the accounts that show up on your Statement of Position or the Balance Sheet. This is where the rubber hits the road. If these accounts’ details are accurate, you can trust the overall financial picture you present to the world.

What is a Statement of Position?

So, what kind of accounts show up on your Statement of Position, and what can you do to make sure the balances are accurate?

Statement of Position is made up of three major types of accounts: assets, liabilities, and net assets (the for-profit world calls that last one “equity”).

- Assets are the things you own: bank and investment accounts, receivables, prepaid expenses, and net fixed assets — all of your capital purchases of things like large equipment, land, buildings, and building improvements, less any accumulated depreciation.

- Liabilities are what you owe: payables, credit card and loan balances, deferred revenue such as membership payments for future years, or advances on government contracts.

- Net Assets are what’s leftover after you subtract your liabilities from your assets. They should come in three (soon to be two) flavors: unrestricted, temporarily restricted, and permanently restricted.

Nonprofit Bookkeeping Tips: Getting Into the Details

How do you know the amounts shown on the Statement of Position are correct? Like the auditors, you need to dig into the details, and you do this by reviewing and reconciling the accounts.

Nonprofit Bookkeeping Starts With Your Bank Accounts

You probably reconcile these each month when you get the statement from your bank. (If you don’t, you should. You ABSOLUTELY should.) These are easy because you know exactly what the balance is supposed to be.

Every accounting software has a reconciliation feature where you enter the date of the statement and the ending balance and proceed to check off the deposits and expenses that have cleared until you reach the point where the variance between what you say cleared the bank matches the bank’s record exactly.

While this is very exciting, it is only the first part of the process. You need to pay attention to the things in your records but not on the bank statement. This is how your nonprofit bookkeeping prevents disasters.

Questions You Should Ask About Your Nonprofit Bookkeeping & Expenses

There are a variety of questions to ask when reviewing your nonprofit’s expenses and bookkeeping, including:

Why haven’t these items cleared the bank?

A year ago, we had a client who noticed that none of their Square deposits were showing up on their bank statement. When they did some research, they discovered that their very trusted volunteer Treasurer had changed the routing so that these payments were going to his personal account.

More often, when you have uncleared deposits in your account, the issue is that someone failed to follow the processes, and income was recorded as both a sales receipt AND a deposit.

Other times, this can happen when PayPal deposits were recorded directly to the bank account, even though they are actually still out with PayPal and haven’t been transferred down yet.

If cash deposits haven’t cleared, it may be a matter of timing. The deposit was recorded on the day the money came into the organization, but it really sits in a drawer somewhere until someone goes to the bank on Friday.

Further Reading: Everything You Need to Know About Donation Processing

Are there checks that haven’t been cleared?

Follow up with those vendors to find out what has happened to the checks, and encourage them to get them to the bank. Ask questions about uncleared debit cards or ACH transactions.

These will typically clear within a day or two. If they haven’t, you need to look into it.

Was the rent paid twice? Are there large checks to vendors you don’t remember working with or to members of the staff?

Often, the transaction has been entered twice, overstating your expenses. Don’t let these hang out there month after month. Figure out what is going on and take action to clean them up.

Your expenses should be about the same every month.. Look for anything you don’t understand.

This is why the person in charge of cutting checks and making deposits should NOT be the person who does the reconciliation. Having two people check each other’s work reduces your error rate and makes your nonprofit bookkeeping as accurate as possible the first time around.

If they must, because your organization is small, set up a process where the bank statements are reviewed monthly by the Treasurer or another board member.

Running Reports & Reviewing Your Nonprofit’s Expenses

The goal is to be very clear on what has run through your bank account and to know why transactions have yet to show up on your statement.

You should start by reconciling your bank accounts, but you shouldn’t stop there. Every month, you should review the details of your other accounts.

1. Run an Open Invoices Report

If you don’t do this regularly, you may be shocked by what you find. Mistakes here often lead to overestimating your nonprofit’s income.

All too often, we enter invoices when we receive a promise or a grant agreement letter but treat it as new money when the check arrives. This means that you have double-counted your income, and the picture painted by your Statement of Activities is not as rosy as you thought.

Other times you may find that you have forgotten to create a receivable for the future portion of a multi-year grant, and by realizing it, you increase your income.

You want the balance in this account to reflect all of the money owed to you accurately.

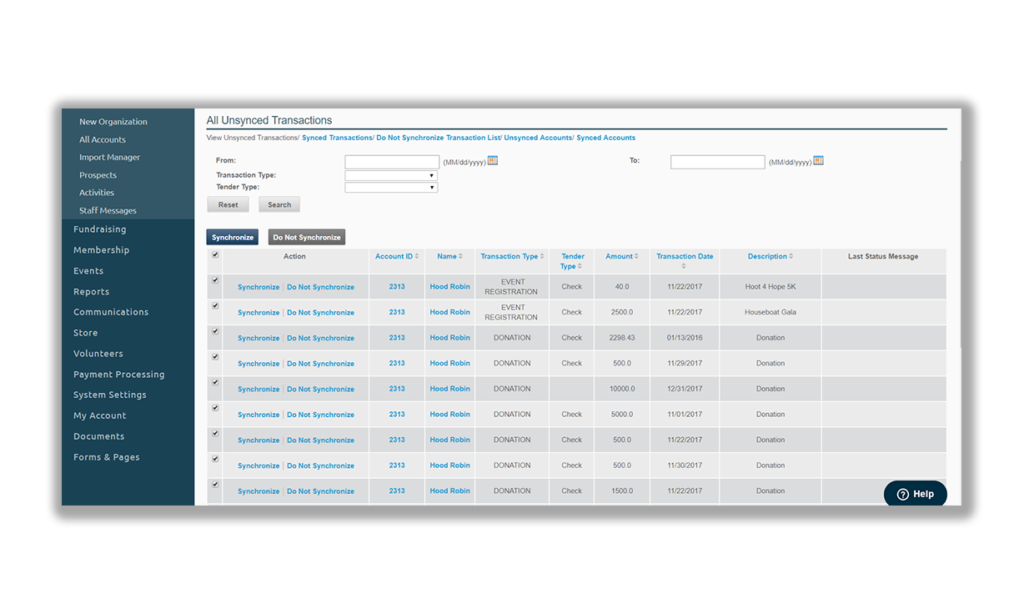

How to Run Transaction Reports in Neon CRM

2. Run an Unpaid Bills Report

The situation here is often much like what we just saw with the receivables. Someone entered a bill and later wrote a check for the same thing, doubling the expense.

Another way this happens is if the organization has incurred expenses but not yet received a bill — that should still be reflected in your Unpaid Bills Report.

3. Dig into Your Prepaid Expenses

Often this is a gigantic pile of goo that no one has looked at in forever. But to complete your nonprofit bookkeeping, you need to dig in. To start, you will need to determine the total associated with each vendor.

How often are these things expensed? If you review and expense items monthly, you can keep a running total for each vendor and take them off your list when the balance gets to zero.

With software like QuickBooks, you can use the Reconciliation tool to clear transactions once the amount for a vendor is fully expensed.

4. Review Your Deferred Revenue

Keep a list of precisely what is going into this account and when it is coming out. You can do this in your software or on an outside schedule. Note that you can only defer Earned Revenue — next year’s tuition, season tickets, or advances on government contracts.

This is NOT the place to put the restricted portions of grants; that must be counted as income when you first find out about it.

5. Maintain a Listing of Your Fixed Assets

Match the amounts on the balance sheet, noting when they were purchased, the initial cost, and the expected life span. This will allow you to calculate and take depreciation, whether monthly, quarterly or at year-end.

Many auditors prefer to help you with this calculation, but you will make nonprofit bookkeeping easier for yourself and your team if you keep a record of the fixed assets you purchase or dispose of.

Reconciliation is About Making Your Life Easier

It is up to you to take the time to review the details of your balance sheet accounts regularly, making sure that you have correctly accounted for all of your expenses and any money owed to you.

Cleaning up old, uncleared amounts in your bank accounts will make it easier for you to REALLY know how much money you’ve got in the bank.

Paying attention to the fine details in the nonprofit bookkeeping process will make your organization Audit-Ready all year long, and your year-end process a dream.

Receive More Nonprofit Bookkeeping and Accounting Advice From Our Consulting Partner Quickbooks Made Easy

And if you’re interested in a new payment processing system, check out Neon Pay, which brings donations, dues, and event revenue into one secure, fully integrated system. Spend less time managing transactions and more time building relationships that drive growth!